The Business Owners Guide to Analyzing Your Small Business Income Statement

Small business owners hate reviewing their financial statements. A combination of it being a reality check and the general disdain for numbers give owners heartburn at even the thought of reviewing an income statement. Small business owners generally don’t have an interest in accounting (only us weirdos do). Besides, most business owners know exactly where their business stands financially by just reviewing their online bank balance every morning, right?

If owners are serious about doing more than lip service of improving their profitability, one of the first steps will be to start reviewing their income statement on a regular basis. The Small Business Development Center in the state of Washington recently put out a presentation on financial discipline for small business owners. In it, they listed the three biggest causes of failure of a small business.

- A Failure to Collect All the Money (Accounts Receivable & Cash Controls)

- A Failure to Manage the Inventory (Physical & Capacity)

- Managing the Business Based on How Much Money Is In the Bank (No Financial Reports)

The presentation they gave later discussed the success rates of businesses based on how often they reviewed their financial reports. Those that only reviewed annually were found to only be 25-35% successful. Those that completed a review monthly had a 75-80% success rate.

Along with passion, the desire to produce a certain amount of income ranks highly with why an entrepreneur usually starts a business. Why then, would an entrepreneur not do all of the things that are known to help them be successful?

Let’s start by defining what an income statement is (also referred to as a profit and loss statement). This statement shows the business’s revenues (usually on top of the page), it’s expenses, and its’ net income or loss over a specified amount of time. It should be noted that net income or loss is not necessarily the amount of cash generated or used by the business. From time to time, businesses will spend cash on items that are not defined as expenses. One example is the principal portion of debt payments is found on the income statement. Another common example is spending money on fixed assets or capital expenditures. Items such as a new truck or piece of equipment will not show up on your income statement. There are also some “non-cash” expenses that are included in your income statement. I won’t go into detail, but know that these may exist.

One of the biggest differences in an income statement from how cash is spent is inventory. Inventory is often included on the balance sheet (and thus not an expense) until it is sold. Once sold, inventory is included in “Cost of Goods Sold”. As such, an increase in inventory during a period often indicates a use of cash that will not be seen on the income statement.

The actual act of generating an income statement is usually very easy. With most accounting software it is just the click of a button. However, the process of generating an income statement can be much more labor intense. This is where most small business owners will use an accountant or bookkeeper. An accountant can make sure that all expenses are categorized properly and make any adjustments to the statement so that it is properly computed.

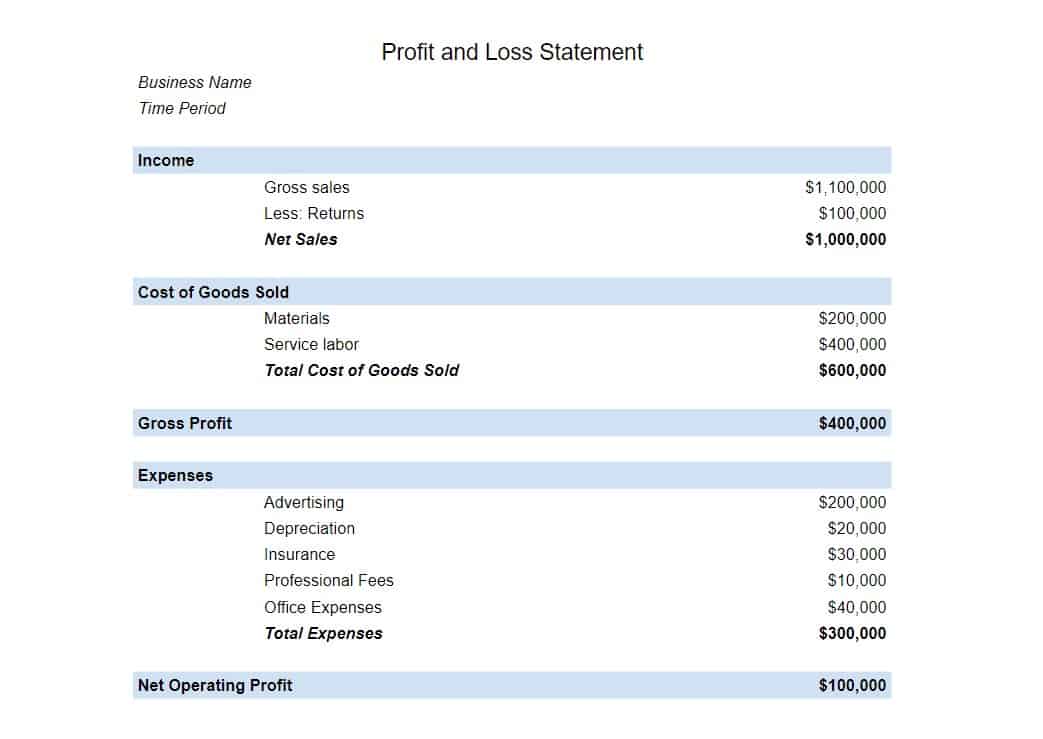

Initially setting up your income statement can be somewhat difficult. Using an accountant to help ensures that the data and presentation will be in the best format possible for you to analyze. The purpose of this article is not to get into a bunch of accounting jargon. However, there can be some issues that are best worked through with your accountant in your initial setup. When set up correctly, a small business income statement is often only 1 to 2 pages long. Here is a quick example of an income statement or profit and loss statement.

Great! Now you know what the income statement is and you have generated it. You are ready to start doing some analysis. Before we get into the “how” let’s discuss the “why”. Why are you analyzing your income statement?

The Goal of Income Statement Analysis

There are a couple of goals when analyzing your income statement. First, you want to make sure the business is performing in accordance with your goals and expectations. Often, the business is performing either above or below your expectations. In either case, you want to strive to understand why. This is also a great opportunity to evaluate all of your expenses to ensure that they are reasonable. Did you mean to spend $1,200 last month on employee gifts (or did you know you did?)?

Budget versus Actual

Most accounting software will allow you to load a budget into it so that you can evaluate budget to actual performance. I would strongly recommend budgeting on a regular basis and that budgeting should be broken into monthly periods. The reason for this is most businesses fluctuate throughout the year. If you are a ski rental company, odds are your operations look drastically different in January than they do June. Most businesses have some sort of seasonality.

When you have a budget loaded into your accounting software, you can quickly produce a report that shows actual expenses compared to budgeted expenses for the month. Why did you only budget $100 for employee gifts but $1,200 was spent? On the flip side, why was your utility bill only $400 when you budgeted $800?

Asking questions like these can help you operate your business most efficiently. If the budgeting process was done correctly, a good amount of time and thought was put into determining what your expenses would be. If you have large variances, you are deviating from your plan. There might be a very good reason for such deviations, but it also might indicate a problem that can be quickly fixed.

Monthly Comparisons

One of my favorite ways to review and income statement is by looking at monthly expenses over a 12-month period. This way I can see how revenue and expenses have fluctuated each month. For instance, maybe the $1200 in gifts was fine because you had not spent any in the previous 12 months and the budget actually called for $2000.

One real-life example is phone/internet bills. Often, as a business owner, you receive some sort of “deal” when you sign up with your provider. That deal is usually only good for 6-12 months and will eventually expire, leading to an increase in rates. Doing a monthly comparison review, you’ll quickly note that this expense almost doubled this month and make plans to address it.

The Cash Flow Statement – The Income Statement’s Younger, Prettier Cousin

The income statement is great to use as a tool for analyzing revenue and expenses and making strategic adjustments to your operations. However, like most business owners, you probably most care about your cash balance. Sometimes the income statement doesn’t correlate well with what is going on with your bank account.

The cash flow statement shows you exactly how your business used and generated cash during the period. Unfortunately, unlike the income statement, this cannot be generated by a click of a button. This statement often takes an accountant to prepare. Fundera has a much more in-depth article on what the cash flow statement is.

With our clients, we like to blend the income and cash flow statements together so that we can more clearly show how their business strategies are impacting their bank account. Doing this certainly isn’t rocket science but is definitely something I would recommend you have your accountant do.

You’re Ready to Review

You now have the basics needed to review your income statement (and possibly cash flow statement). I would strongly recommend reviewing with your bookkeeper or accountant as they are trained and have experience in pointing out areas for you to consider.

If you would like to discuss your goals and how Krieger Analytics can help your business grow to achieve them, contact us now. What are you waiting for? Phone calls are always free!