Why your income statement doesn’t match your bank account

I see this almost every time I start working with a new client. An agency owner sits down on a Monday morning to review April’s books. The P&L shows $78,000 in net profit. The bank account shows $4,200. Both numbers are correct. Neither is wrong. That is the problem. Your income statement and your bank account measure two completely different things, and under accrual accounting (the method that records revenue when earned and expenses when incurred, regardless of when cash actually moves) they almost never produce the same number.

This isn’t a bookkeeping error. It’s a feature of how accounting works, and most owners don’t learn it until they’re staring at it. According to the Federal Reserve’s 2025 Report on Employer Firms, 51% of small employer firms cited uneven cash flows as a financial challenge — and a lot of that confusion starts here.

Profit and cash measure different things

Your income statement answers one question: did the business earn more than it spent during this period? It records revenue when you invoice a client, not when they pay. It records expenses when you receive a bill or recognize a cost, not necessarily when cash leaves the account.

Your bank account answers a different question: how much cash came in and went out? It doesn’t care whether a client has paid yet. It doesn’t care whether last month’s rent was prepaid or whether a loan repayment came through. Every dollar moving through the account shows up there in real time.

Cash basis accounting (records income and expenses only when cash is received or paid) would produce numbers that align more closely with the bank. Most businesses over $1M in revenue use accrual accounting instead, because it gives a more accurate picture of financial performance across time. The trade-off is this: your P&L can show strong profit while the bank account looks thin, and vice versa.

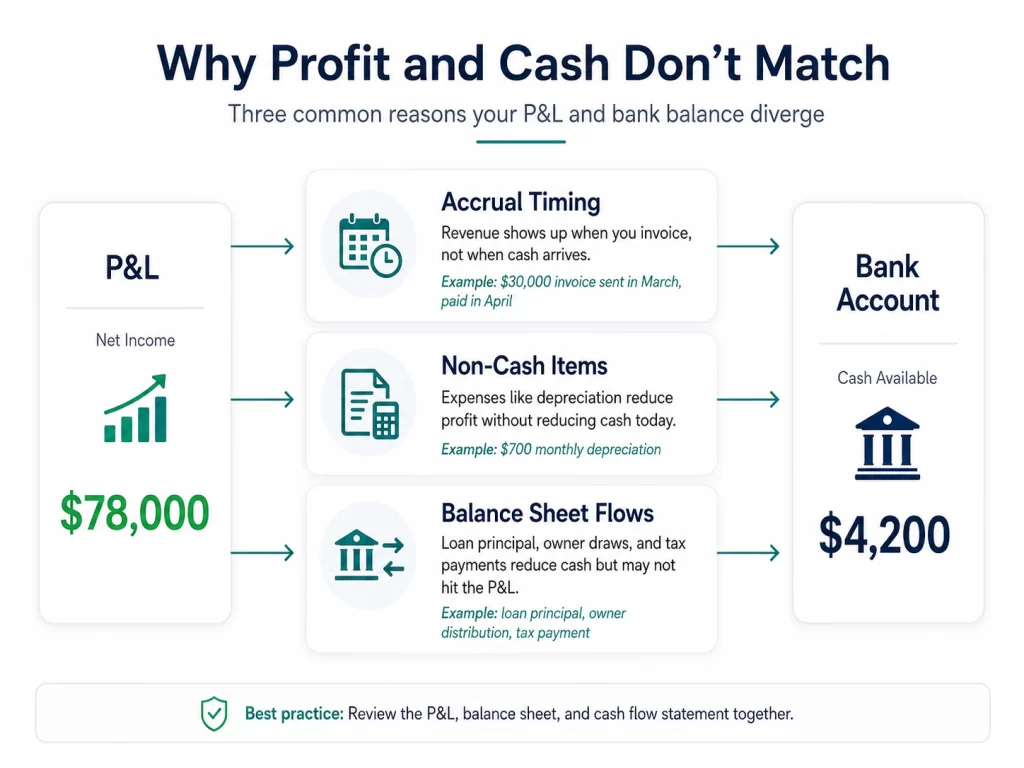

Three things that pull the numbers apart

Three mechanics account for most of the gap between what your income statement shows and what’s sitting in the bank.

Accrual timing. You finish a $30,000 consulting engagement in March and send the invoice. March’s P&L includes $30,000 in revenue. If the client pays in April, the bank account shows $0 from that client in March. The revenue is real. The cash just hasn’t arrived yet. This is the most common source of confusion for service businesses because their receivables can stack up fast. Accounts receivable (money owed to the business by clients for work already completed) sits on the balance sheet, not in the bank.

Non-cash items. Your business buys $84,000 in equipment. You spread the cost across 10 years through depreciation (a non-cash accounting expense that reduces P&L profit but does not reduce the bank account). In month one, the P&L takes an $700 depreciation hit. The bank account lost $84,000 when you bought the equipment, not $700 per month. Every month after that, the P&L expense exists but no cash leaves the account. By the end of year one, the P&L has recorded $8,400 in depreciation expenses that don’t appear anywhere in your bank transactions.

Balance sheet flows. This is the one most owners miss entirely. Loan principal repayments, owner distributions, and tax prepayments all pull cash out of the bank account without touching the P&L. A $2,000 monthly vehicle loan payment hits the bank in full every month. Only the interest portion (say, $180) shows as an expense on the P&L. The remaining $1,820 in principal repayment reduces the bank balance, reduces the loan liability on the balance sheet, and disappears from the P&L entirely.

| Transaction | P&L impact | Bank account impact |

|---|---|---|

| Invoice sent for $30,000 project, payment not yet received | $30,000 revenue recorded | No cash received yet |

| Client pays $30,000 invoice from last month | No new revenue recorded | $30,000 cash received |

| Equipment depreciation ($700/month on $84,000 asset) | $700 expense recorded | No cash leaves account |

| Monthly loan payment ($2,000 total: $180 interest + $1,820 principal) | $180 interest expense recorded | $2,000 leaves account |

| Owner distribution ($8,000) | No expense recorded | $8,000 leaves account |

| Tax estimated payment ($6,500) | No expense recorded (if already accrued) | $6,500 leaves account |

The table above shows six transactions common to a $1M to $5M service business. Three of them take cash out of the bank without any P&L impact. Two of them hit the P&L before cash moves. Only one (the payment received on a prior invoice) affects the bank without creating new P&L revenue.

What the mismatch is actually telling you

The gap between your P&L and your bank account is not a problem by itself. It’s information. I’ve sat across the table from agency owners who had been staring at this exact gap for six months before we worked through it together — and in most cases, the numbers weren’t wrong, they just hadn’t been interpreted. The question is whether anyone at your business is reading them.

When accounts receivable are growing because you’re invoicing more clients, a timing gap is expected and healthy. That $78,000 in net profit is real — it just hasn’t converted to cash yet. A 30-day receivables cycle is normal for most agencies and consulting firms. A 60-day cycle is a collections problem worth addressing.

When the gap is driven by balance sheet flows (loan principal, owner distributions, prepaid taxes), the P&L isn’t wrong. It just doesn’t tell the full story. The financial statement that bridges the income statement and the bank account is the cash flow statement (the report that tracks actual cash inflows and outflows, organized into operating, investing, and financing activities). Most small business owners who use a bookkeeper get a P&L and a balance sheet each month. Few get a cash flow statement, and fewer still have anyone explaining what it means.

That oversight gap is where most of the confusion lives. Our cash flow statement primer walks through how the statement works and how to read it alongside the P&L. If you haven’t seen one for your business, that’s the starting point.

When the gap signals something is actually wrong

A timing gap that resolves in 30 to 60 days as receivables come in is normal business. A persistent gap where the P&L consistently shows profit while the bank account stays thin is a different situation.

A few patterns worth taking seriously:

- Receivables aging beyond 60 days with no follow-up process: revenue is real on paper but collection is becoming uncertain.

- Owner distributions consistently exceeding net income: the business is profitable on paper but the owner is pulling more than it earns.

- Loan principal repayments consuming a significant share of operating cash: the business carries debt service that doesn’t show in the P&L profit figure, so the “real” retained cash is much lower than the income statement suggests.

- Tax liabilities not accrued properly: cash leaves in a lump sum at estimated tax time with no prior P&L signal.

The IRS requires businesses above certain revenue thresholds to use accrual accounting (see IRS Publication 538: Accounting Periods and Methods for the specifics). That requirement exists because accrual accounting provides a more accurate picture of business performance. The trade-off is that the P&L alone becomes an incomplete tool for managing cash.

Good cash management for small business owners means tracking all three statements together: P&L for performance, balance sheet for position, cash flow statement for the actual movement of money. Most $1M to $5M businesses have someone doing the bookkeeping but no one connecting those three documents into a coherent picture of what the business is doing.

If the numbers haven’t made sense in a while, that’s the actual problem

The income statement and bank account will almost never match, and that’s fine. What isn’t fine is running a business for months without understanding why they’re different or what the gap is signaling about cash availability, receivables timing, or debt service load.

In my experience, when an owner has been confused about this for more than a quarter, the issue usually isn’t the accounting. It’s that no one is interpreting the accounting for them. A bookkeeper captures transactions accurately. Knowing what those transactions mean for your cash position three months from now is a different job.

If that’s the gap you’re looking at, it’s worth a conversation about what outsourced CFO services for small businesses actually looks like at your revenue level.

Frequently asked questions

Why does my income statement show profit when my bank account is negative?

Under accrual accounting, revenue is recorded when earned (when you invoice a client), not when cash is received. If you have significant accounts receivable — clients who owe you money for completed work — the P&L shows that revenue while the bank account doesn’t yet. Add loan principal payments, owner distributions, and tax prepayments (none of which appear as P&L expenses in most cases), and it’s common to show strong profit while the bank looks thin.

What is the difference between net income and cash in the bank?

Net income is an accounting measure: total revenue minus total expenses for a period, calculated under accrual rules. Cash in the bank is a real-time count of what’s actually there. They diverge because of timing (revenue earned but not yet collected), non-cash items (depreciation reduces net income without moving cash), and balance sheet activity (loan payments and owner draws reduce cash without appearing as expenses on the P&L).

Can a business be profitable but run out of cash?

Yes. This is one of the more common ways small businesses fail. If a business is growing fast, invoicing outpaces collections, and cash is consumed by equipment purchases, loan service, or owner draws, the P&L can look healthy while the business can’t cover payroll. Profitable businesses run out of cash when no one is managing the difference between what the income statement shows and what the bank actually holds.

Does accrual accounting make my bank balance look wrong?

No. Your bank balance is always accurate — it shows exactly what cash is available. Accrual accounting makes your P&L show revenue and expenses at different times than cash moves. The bank balance and the P&L are both correct; they just measure different things. The cash flow statement is the tool that reconciles them.

What is the cash flow statement and how does it connect to the P&L?

The cash flow statement tracks every cash inflow and outflow during a period, organized into three categories: operating (day-to-day business), investing (equipment, assets), and financing (loans, owner equity). It starts with net income from the P&L and adjusts for every item that caused the two numbers to diverge: changes in receivables, depreciation, loan activity, and owner distributions. The ending balance on the cash flow statement should match the bank account. See our cash flow statement primer for a step-by-step walkthrough.