How to Pay Yourself as a S-Corp Owner

How to Pay Yourself as a Consulting Firm Owner

A client came to me generating $2.2 million in annual revenue. She was paying herself an $85,000 salary and pulling the rest as distributions, with no formal documentation to back the split. Her CPA had reviewed the returns and told her she was “fine.” She wasn’t fine. Her salary was too high relative to what the IRS would accept as a genuine market rate for her role, which meant she was running unnecessary payroll taxes through distributions that she could have structured to avoid. The gap between what she was paying and what she should have been paying ran $8,000 to $15,000 per year. Owner compensation at $1M to $5M in revenue is a tax planning decision. It is not a question of payroll mechanics or how your bookkeeper sets up the paycheck.

What “Paying Yourself” Actually Means at $1M to $5M

The method you use to pay yourself depends entirely on your entity structure, and the three approaches are not interchangeable.

If you operate as a sole proprietor or a partnership, you take an owner’s draw — a withdrawal of business equity that isn’t treated as a wage and isn’t subject to withholding. The catch is that all net profit from the business flows to your personal return regardless of what you actually draw, and you pay self-employment tax (the 15.3% combined Social Security and Medicare tax that sole proprietors and partners pay in place of the employer/employee split) on all of it. At $300,000 in net profit, that’s over $42,000 in self-employment tax before you reach income tax.

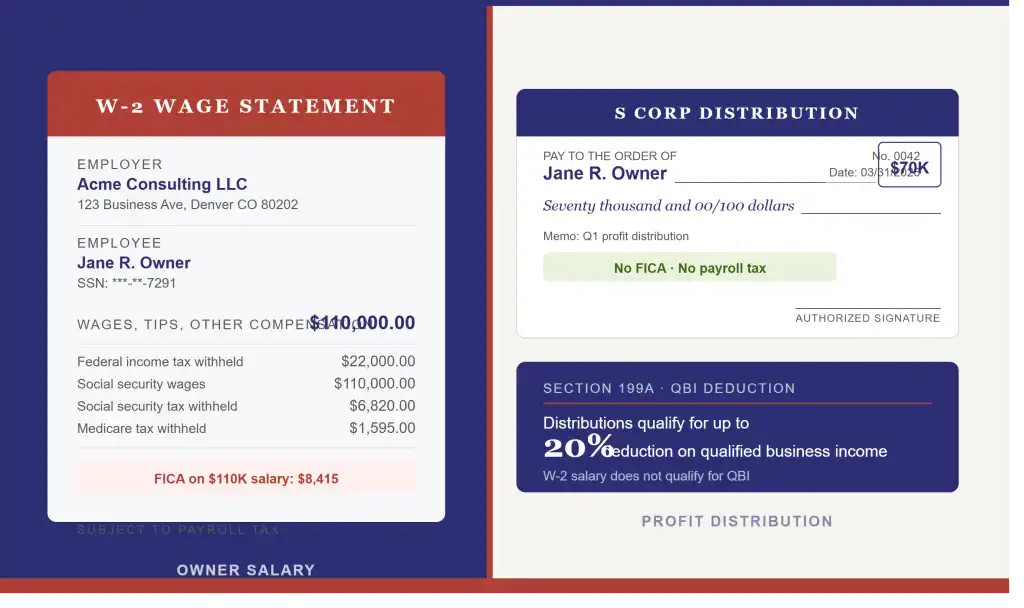

S corporations operate differently. An S corp requires you to pay yourself a W-2 salary first. Anything left over can come out as a distribution. Only the W-2 salary portion is subject to payroll taxes. The distribution is not. That distinction is where the planning opportunity lives.

C corporations require a W-2 salary for owner-employees. The corporation pays its own taxes at the corporate rate, and dividends to shareholders face a second layer of tax. For most consulting firms and agencies under $5M in revenue, C corp status adds cost and complexity without meaningful benefit. The discussion below focuses on S corps because that’s the structure where compensation decisions have the most direct impact on annual tax liability.

The S Corp Distribution Decision: When It Matters, When It Doesn’t

The S corp structure only makes financial sense above a certain profit threshold, and that threshold matters before you build a compensation strategy around it.

Below roughly $60,000 in annual net profit, S corp compliance costs — payroll processing, a separate corporate return, potential state fees — tend to consume what you’d save in payroll taxes. The math doesn’t work. Above that level, it shifts. At $180,000 in net profit, the difference between taking everything as a W-2 salary versus splitting it 60/40 between salary and distributions looks like this:

| 100% W-2 Salary | 60/40 Salary/Distribution Split | |

|---|---|---|

| W-2 salary | $180,000 | $108,000 |

| S corp distribution | $0 | $72,000 |

| Payroll tax (employer + employee) on salary | ~$27,540 | ~$16,524 |

| Payroll tax on distribution | $0 | $0 |

| Estimated annual savings | — | ~$11,200 |

Figures are directional examples based on the 2026 payroll tax rate of 15.3% (combined employer and employee share) applied to wages below the Social Security wage base ($176,100). Confirm with your CPA before making decisions based on these numbers.

There’s a second benefit worth naming here. The QBI deduction (the qualified business income deduction under Section 199A, which allows pass-through business owners to deduct up to 20% of qualified business income from taxable income) applies to S corp distributions but not to W-2 salary. That deduction is income-tested and has phase-outs depending on business type, but for consulting firms whose owners are under the threshold, distributions increase the QBI base. A higher distribution proportion means more income eligible for that deduction.

What Counts as a “Reasonable Salary” for a Consulting Firm Owner

The IRS requires S corp owner-employees to pay themselves a salary comparable to what an outside hire would earn doing the same work. This is the reasonable compensation standard, and it’s the first thing an examiner asks about in an S corp audit.

There are three methods the IRS accepts for establishing a defensible salary.

The most common is the market rate approach: look at what employers pay someone with equivalent responsibilities. The Bureau of Labor Statistics Occupational Employment and Wage Statistics program (BLS OES data) puts the median annual wage for management consultants at $100,000 to $130,000 nationally. That’s your anchor for most firms. If you’re generating $2.5M in revenue with a team of 12, $68,000 isn’t defensible. $110,000 probably is, documented with the BLS data.

The second method is the cost approach: estimate what it would cost to hire two or three people to cover everything you actually do in the business — operations, sales, delivery, finance. This approach tends to push salaries higher and works well when your revenue is growing faster than comparable market wages.

The third is the income approach: base your salary on a portion of the business’s net profit, typically following industry norms for owner-operator compensation. It’s less commonly used in practice because it can produce very high salaries when profit is strong, which is the opposite of what most S corp owners want.

IRS Publication 15-A is the foundational reference for employer tax obligations and compensation documentation requirements. The reclassification risk — where the IRS recharacterizes distributions as wages and assesses back payroll taxes, interest, and penalties — traces to IRS Revenue Ruling 74-44. Whatever methodology you use, document it annually. A one-page memo in your records is far better than trying to reconstruct the rationale three years later when the IRS asks.

The CFO Angle: Why Most Owners Get This Wrong

I work through owner compensation with nearly every new client I take on, and the pattern is consistent. Most owners at this stage have a bookkeeper recording transactions and a CPA filing the return. Nobody in that setup is thinking about the middle layer: structure, strategy, and the ongoing review that keeps the structure current.

The two most common mistakes I see are not revisiting compensation since the business crossed $1M (the salary that made sense at $800,000 in revenue isn’t necessarily right at $2.5M) and changing salary at tax time based on a single suggestion without any documented rationale. Neither of those holds up if the IRS asks. The IRS doesn’t accept “my CPA suggested it” as a methodology.

Owner compensation also has direct downstream effects on cash flow that a bookkeeper isn’t positioned to model. The right salary-to-distribution ratio affects quarterly estimated tax payments, cash reserves, and the QBI calculation. These decisions interact. For a closer look at how compensation timing connects to cash positions across the year, see our guide to cash flow management for owner-operators. Owners who are also evaluating whether their current business model still makes financial sense will find related context in financial feasibility for your business.

When to Do the Review

If you haven’t looked at your owner compensation structure since you crossed $1M in revenue, the review is overdue. The right time to do it is before next year’s return is filed, not after the IRS sends a notice.

The mechanics of S corp election, salary documentation, and distribution planning aren’t complicated once someone walks you through them. What most owners need isn’t a one-time tax opinion but an ongoing relationship where compensation gets reviewed annually alongside cash flow, growth plans, and what the business actually needs from you. That’s exactly what we work through with clients through our outsourced CFO for small businesses engagements. If you want to pressure-test your current structure, that’s a good place to start.

Frequently Asked Questions

Can I pay myself both a salary and an owner’s draw from the same business?

It depends on your entity structure. An S corp owner-employee takes a W-2 salary and can take additional distributions from profits, but those aren’t called “draws” in the S corp context. A sole proprietor can’t pay themselves a salary at all — there’s no legal mechanism for it — but can take draws freely. The two methods come from different structures. If you’re operating as an S corp, the right question is how to split between salary and distributions, not whether to add a draw on top.

How much should a consulting firm owner pay themselves?

The IRS requires S corp owners to pay a “reasonable salary” comparable to what an outside hire would earn for the same work. For a management consultant running a $1.5M to $5M firm, Bureau of Labor Statistics data puts the national median for management consultants at $100,000 to $130,000 annually. Your specific number should reflect your actual responsibilities, the size of your firm, and what you can document with comparable market data. A salary that’s too low triggers IRS reclassification risk; one that’s too high leaves payroll tax savings on the table.

What happens if my S corp salary is too low?

The IRS can reclassify distributions as wages and assess back payroll taxes, plus interest and penalties. This risk traces to IRS Revenue Ruling 74-44, which established that payments to shareholder-employees labeled as distributions but functioning as compensation for services are subject to employment taxes. The exposure is real: back taxes on several years of distributions, compounded by interest and a potential accuracy-related penalty. A defensible salary methodology, documented annually, is the standard protection.

Is an owner’s draw considered income for tax purposes?

Yes, but not in the way a W-2 salary is. A sole proprietor or partner doesn’t pay income tax directly on draws. Instead, all net profit from the business is included in the owner’s taxable income for the year, whether drawn or not. The draw is just a movement of money from the business account to the personal account. Self-employment tax (15.3% on net earnings) applies to all of that net profit regardless of what was actually withdrawn.

When should I elect S corp status for my consulting firm?

The general threshold where S corp election starts making financial sense is around $60,000 to $80,000 in annual net profit, when payroll tax savings begin to outpace the compliance costs of running a corporate return and payroll. Below that level, the compliance overhead — separate return, payroll processing, state fees in many jurisdictions — tends to cancel out the savings. Above it, the math shifts. The election itself has timing rules: for the S corp election to take effect for a given tax year, Form 2553 generally needs to be filed by March 15 of that year (or within 75 days of formation for a new entity). Talk to a CPA before electing, not after.